Where You Sit Changes Everything

With the World Cup underway, even we Canadians are calling it football. Offence sells tickets, defence wins championships. In private credit, yield gets the attention. Protecting capital is what determines the outcome.

We have written about the capital stack before. We will likely write about it again. What is happening across parts of the private credit market keeps making the case for why it matters.

Questions about valuation opacity, the growing use of payment-in-kind structures, the consequences of deploying capital faster than discipline allows. These are not abstract industry debates. They point back, every time, to the same foundational question: where does the lender actually sit, and what is backing the loan?

This is the first in a three-part series. Part Two will go deeper into what we lend against, the collateral itself, and why not all assets are equal. Part Three will address what happens when things go wrong, and why our structure is built so that conversation rarely applies to us.

The capital stack is not complicated. But it is easy to overlook.

Every business that borrows money carries a hierarchy of obligations. Senior secured lenders sit at the top, with first legal claim on the borrower’s assets if something goes wrong. Below them are junior secured and unsecured creditors, then preferred equity, then common equity holders, who are last in line in any recovery scenario.

Higher position means stronger repayment priority. In a stress scenario, a senior secured lender is made whole before anyone else sees a dollar.

Garrington focuses exclusively on senior secured lending. This shapes every decision we make.

Priority claim is only meaningful if there is something to claim against.

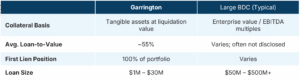

A senior secured position against enterprise value (the implied worth of a business based on its earnings multiples) is a very different thing than a senior secured position against tangible, identifiable, realizable assets. Both may appear in the same column of a capital stack diagram. They do not carry the same protection.

Enterprise value is a function of assumptions. It depends on revenue projections, margin expectations, market multiples, and conditions that change. When credit markets tighten or a business disappoints, enterprise value can compress quickly. A senior position against an enterprise value of $50 million becomes a much less comfortable position when that value falls to $30 million.

Tangible assets behave differently. Inventory and equipment have a liquidation value. Receivables represent money that is contractually owed. Real estate can be appraised and sold. These assets can be valued independently of a business’s outlook, monitored continuously, and if necessary, liquidated to recover capital.

We lend against assets we can see, value, and recover.

Our portfolio is built on senior secured loans backed by tangible collateral: equipment, accounts receivable, inventory, real estate, and other business assets with identifiable, verifiable value. We assess the liquidation value of those assets before we lend. We place a perfected first lien on them. We set conservative advance rates and build in covenants that give us visibility and control throughout the life of the loan.

Our weighted-average loan-to-value ratio has historically ranged between 50% and 70%, currently sitting at approximately 55%. For every dollar deployed, there is meaningful collateral coverage underneath it, calculated not on optimistic projections but on what those assets would realistically return in a liquidation scenario.

That distinction matters most when markets become difficult.

Senior Secured Positioning vs. Typical Private Credit

The market keeps reminding us why this matters.

Recent years have surfaced real concerns across the private credit industry: complex structures, crowded sectors, questions about how valuations are calculated and reported, and a growing use of payment-in-kind arrangements that defer cash interest in ways that can obscure borrower health.

These are the natural consequence of capital flowing into a market faster than disciplined deployment can absorb it. When the pressure to deploy outpaces the discipline to select, structures loosen. Advance rates creep up. Enterprise value becomes an increasingly generous measure of coverage.

We have stayed in a part of the market where those pressures are less acute. Sub $20-30 million loan sizes, below the threshold of the large direct lending platforms, in a fragmented market with less centralized competition and more room for careful underwriting. Selectivity is itself a source of return.

Final Thought

Where you sit in the capital stack determines what you are owed and how realistically you can collect it.

For us, senior secured positioning backed by tangible collateral is not a feature we highlight in a presentation. It is the structural premise of everything else we do. The consistency of our returns, the stability of our loan-to-value ratios, the near-zero impairment history. None of it exists without this foundation.

In Part Two, we will go deeper: not just what collateral we take, but how we think about it, how we monitor it, and why understanding the difference between assets that hold their value and assets that erode quietly under pressure is one of the most important disciplines in private credit.

Subscribe

Have our blog delivered directly to your inbox: