A Deeper Look At Factoring and its Investment Potential

Last week, we introduced invoice factoring—a key strategy in our portfolio that provides businesses with immediate liquidity by unlocking cash tied up in receivables. If you missed it, click here to catch up. This week, we’re going deeper, focusing on how factoring works and why it presents an attractive, risk-mitigated opportunity for our investors.

Businesses across a wide range of industries—from manufacturers managing supplier costs to distributors balancing inventory, transportation firms covering fuel expenses, and service providers handling day-to-day operations—use factoring to keep cash flowing. Whether in construction, wholesale trade, healthcare, or any sector that extends payment terms to clients, factoring provides stability, ensuring businesses meet obligations and seize growth opportunities. Our approach goes beyond providing liquidity—it’s about optimizing cash flow, reducing risk, and delivering strong, asset-backed returns for investors.

How does it Work?

It sounds simplistic to say, “Find a company that has an invoice for a product delivered or a service rendered and purchase it,” but it is almost that simple.

Across Canada and the U.S., where we operate, the rules and regulations established regarding factoring are long-standing and fairly favourable to this type of financing.

Facilities are structured as true purchases, where the sale is legally binding, and the Factor has ultimate rights to the payments from the Seller’s (client’s) Debtors.

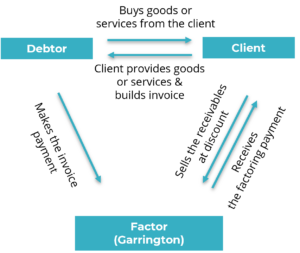

Fig 1. Invoice factoring scheme

In addition to having a true purchase of receivables, we also take senior lien security to solidify our rights to the accounts and proceeds of that client.

Why Would Our Client’s Customers Pay Us?

Part of the true sale process of the receivable, and a critical aspect of factoring, is notifying the client’s customer (Debtor) that we have purchased that invoice. This is done through a Notice of Assignment and Sale of Accounts, whereby the Debtor is advised of the sale and notified of where their payments are required to be sent. This notice stays in place for the duration of the client’s relationship with the Factor and can only be revoked by the Factor.

Further, Debtors are advised that failure to pay where they are instructed would not be considered a release of their payment liability.

What this means is that should funds be directed elsewhere and not forwarded to the Factor, the Factor has the legal right to pursue the Debtor for payment, and the Debtor would be forced to pay twice.

While such measures do not often happen, many Factors have had to use these legal tools to recover funds and have been successful.

Interest vs. Purchase Price – How We Charge

Due to the nature of the transaction, this is not a loan, so we do not charge interest on the funds advanced.

As a discounted purchase, we charge a discount fee based on the face value of the receivable. This fee is represented as a percentage of the value for a certain amount of time; for example, 1.25% for 30 days. We then distribute that fee over 30 days and continue to charge on that invoice for each day it surpasses that initial period until that invoice is paid, for example: 0.042% per day for every day outstanding starting on the 31st day.

Reserves

Factors typically hold reserves back at purchase, somewhere in the 5-25% range. These reserves protect the Factor from instances where the invoice is paid for less than the face value due to deductions, discounts, and returns—what we call dilution.

These reserves are held until an invoice is paid and then returned to the client on a scheduled basis.

Recourse

A factor will only allow a receivable to remain unpaid for a certain amount of time, and this is where recourse comes into play. Generally, set at 90 days, if an invoice becomes available for recourse, the client is required to repurchase that receivable from the Factor.

The repurchase is made either by way of replacement with new receivables, the use of available cash reserves or payment in cash.

How Do We Factor Safely?

Given the favourable regulations and safeguards in place to Factor successfully, how do we actually put it into practice and do it safely? Our next blog post will explore exactly that!