The Four Pillars of Strength – Pillar #2 – Robust and Efficient Underwriting: The Backbone of Smart Lending

Welcome to the second installment of our Four Pillars of Strength blog series. In private credit, success hinges on more than opportunity—it demands precision, discipline, and a deep understanding of risk. Robust and Efficient Underwriting is at the heart of Garrington’s investment philosophy, a critical process for us to ensure we balance opportunity with protection.

Step behind the curtain to see how our underwriting approach combines rigorous analysis, industry expertise, and operational efficiency to identify high-quality opportunities that drive the North American economy, while safeguarding investor capital. Discover why this pillar is not just a function but the backbone of smart lending and a key driver of our consistent, uncorrelated returns.

Garrington Investment Philosophy – Garrington Four Pillars of Strength

Private lending to SME businesses in North America, primarily in loan sizes under USD $30 million can provide excellent risk adjusted returns relative to other asset classes WHEN MANAGED APPROPRIATELY

The key to having successful clients is selecting the right potential Borrowers and learning everything we can about them, their business, their collateral, and how they operate. Couple that with our seasoned and experienced Investment Committee, with a number of members having more than 25 years of experience in the alternative lending industry, we hold the recipe for success. We have the skill to focus in on the risks involved in each transaction and to structure facilities that meet the Borrower’s needs and mitigate risks for our stakeholders.

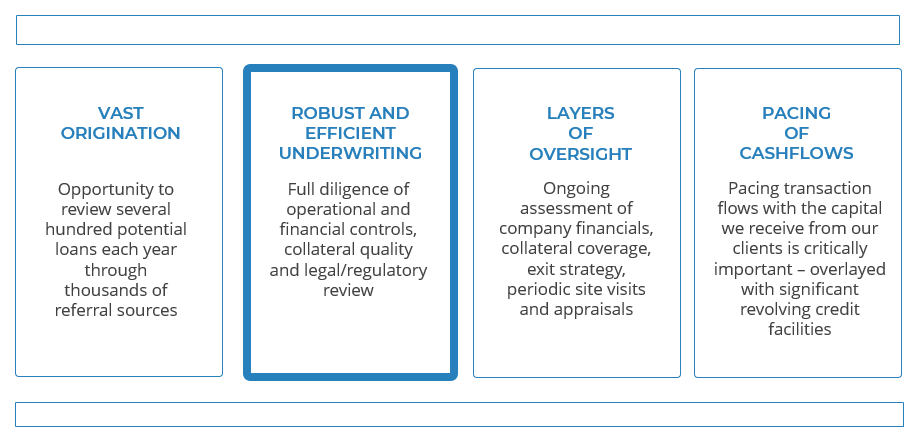

Any robust underwriting requires intense scrutiny and detailed work with a potential Borrower. The way we assess a transaction can be broken out into four parts:

- Collateral

It would seem strange to think that the first thing we consider when reviewing a potential loan is, “How do we get out?” However, that is the backbone of what we do. It is the collateral that we rely on to recuperate our funds in the event something goes wrong. We do that by using the knowledge of our team along with strong, professional third-party partners, such as field examiners and appraisers. These professionals take deep dives into the collateral to understand how the assets behave in the normal course (e.g., accounts receivable, inventory, loan portfolios), the condition and wear and tear of the assets (e.g., equipment, real estate), and the ultimate Liquidation Value of those assets.

When dealing with assets like equipment and inventory, we collaborate with professional firms that specialize in liquidating these assets and possess specific expertise in the relevant industry. These partners bring firsthand experience, often having successfully sold similar assets in the recent past. We rely on these values to feel comfortable in knowing that our advanced funds will be highly likely to return in the event of a default. - Operational Controls

Meeting with the individuals who operate the business we’re contemplating lending to is critical. It’s an opportunity to understand what they want to achieve through our funding, such as executing a turnaround plan, growth plan, etc. We want to know what they’ve been through, what they’re currently experiencing, and where they are planning to be. Will our funding assist in that plan and provide value at the level we’ve determined through our valuation process? All of these things help us lay a solid foundation as a lender, determining if we can be a partner to them and assist them in their success. - Financial Controls

Although we adequately prepare ourselves for the worst-case scenario, a liquidation, we strive, from the outset, to really review our potential Borrowers from a viability perspective. Asking ourselves: are we likely to have a client in 3, 6, 9, or 12 months, or is it possible that they will falter? Our skilled teams perform financial analysis on historical, current, and projected results, digging in and asking questions, reviewing reasonability, and looking for detailed explanations of anomalies and trends. Particularly key is reviewing projections and key drivers to ensure that: 1. They make sense, and 2. Applying our debt does not adversely impact the company but can clearly show how it can provide value in achieving those results. - Legal/Regulatory Review

Documenting and properly securing a transaction is the last step before funding. We pride ourselves on our ability to structure and negotiate documents, no matter the complexity. To do this, having strong outside legal counsel is very important, and working with those partners and firms with significant experience in this industry is critical. They are the last line of defense to review and ensure that our documentation represents the intended structure, adequately protects us, and that our security is appropriately registered.

The four key elements outlined, along with the extensive reviews we conduct, form the foundation of a strong client-lender relationship. We understand that when we engage with a new potential client, they are about to begin a thorough diligence journey with us. However, we believe that the insights we gain from this process and the partnership we develop will significantly enhance their experience as our client. As a partner lender, our goal is to provide effective solutions and contribute to the success of the businesses we collaborate with.

If you’d like to discuss, please feel free to contact us:

investors@garringtonprivatecredit.com